Commercial Real Estate Financing: Best Loans for 2026

Commercial real estate financing in 2026 gives property investors more loan options than ever, but the right choice depends on your deal strategy, property type, and borrower profile. Whether you are acquiring a stabilized office building, repositioning a retail center, or building from the ground up, the financing you select directly affects your returns, timeline, and risk exposure.

The best commercial real estate loan is not the one with the lowest rate; it is the one that aligns with your property stage, exit strategy, and qualification strengths. A bridge loan that closes in two weeks may outperform a conventional mortgage if timing drives your deal. An SBA 504 loan with a 10% down payment may preserve capital better than a traditional bank loan requiring 25% down.

This guide breaks down every major loan type available to property investors in 2026, explains how to match financing to your specific deal, covers current rates and terms, walks through qualification standards, and helps you avoid the most common mistakes in commercial real estate lending.

Key Takeaways

Your loan type should be driven by property stage and deal strategy, not just rate, with options ranging from SBA and conventional bank loans to bridge, CMBS, hard money, and portfolio lending.

Qualification hinges on metrics like DSCR, LTV, credit score, and borrower experience, and these vary significantly across lender types.

Structuring your financing around a clear refinance or exit plan prevents costly surprises from balloon payments, prepayment penalties, and recourse exposure.

Best Commercial Real Estate Loan Options In 2026

The commercial lending market in 2026 includes conventional bank financing, government-backed programs, short-term capital solutions, and private lender products. Each loan type serves a different investor profile, property condition, and timeline. Rates for commercial mortgages currently start near 5.36%, but the spread between loan types can be significant depending on leverage, term, and risk.

Conventional Commercial Loans From Traditional Banks

Traditional bank loans remain the baseline for commercial real estate financing. These conventional commercial loans typically offer 5- to 20-year terms, competitive fixed or variable interest rates, and amortization periods up to 30 years.

Traditional banks favor stabilized, income-producing properties with strong cash flow. Expect to provide a 20% to 30% down payment, demonstrate a debt service coverage ratio (DSCR) of at least 1.25, and show solid borrower financials.

The trade-off is speed and flexibility. Traditional bank financing involves a longer underwriting process, stricter documentation requirements, and less willingness to lend on transitional or value-add properties. If your deal is straightforward and your credit profile is strong, a conventional commercial loan often delivers the lowest cost of capital.

SBA 504 And SBA 7(a) Loans For Owner-Occupied Properties

SBA loans are designed for owner-occupied commercial properties and offer some of the most favorable terms in the market. Both programs cap at $5 million to $5.5 million and require a personal guarantee.

SBA 504 loans provide long-term, fixed-rate financing with down payments as low as 10%. They work best for purchasing or improving fixed assets like buildings, land, and equipment. The structure involves a Certified Development Company (CDC), which adds complexity to the closing process.

SBA 7(a) loans are more flexible in their uses. You can acquire, refinance, or improve commercial property with terms up to 25 years. Approval takes longer than conventional channels, but the lower equity requirement helps preserve working capital.

Choose the SBA 504 when you want rate certainty on a property purchase. Choose the SBA 7(a) when you need broader flexibility or plan to refinance existing debt.

Bridge Loans For Transitional And Time-Sensitive Deals

Bridge loans provide short-term capital, typically with terms of 6 to 36 months, for investors who need to move quickly or are working with properties in transition. Bridge financing is ideal when you are acquiring a property before permanent financing is in place, stabilizing a building to qualify for better terms, or competing against all-cash buyers.

Interest rates on bridge loans run higher than conventional options, often ranging from 7% to 12% or more. Most are interest-only during the term, keeping monthly costs manageable while you execute your business plan.

The key risk is your exit strategy. You need a clear plan to refinance into permanent financing or sell the asset before the bridge loan matures.

CMBS And Conduit Loans For Stabilized Assets

CMBS loans, also called conduit loans, are commercial mortgages pooled together and sold as securities to investors on the secondary market. They are typically non-recourse, fixed-rate loans with 5- to 10-year terms and competitive interest rates.

CMBS financing works best for stabilized properties with predictable cash flow and strong occupancy. These loans often offer higher leverage than bank financing, with LTV ratios up to 75%.

The downside is rigidity. CMBS loans come with strict prepayment structures, including defeasance or yield maintenance. Modifications after closing are difficult because the loan has been securitized. If you value flexibility or plan significant property changes during the loan term, CMBS may not be the right fit.

Hard Money And Private Lender Financing

Hard money loans are asset-based, meaning the lender focuses primarily on the property's value and after-repair value (ARV) rather than the borrower's credit score or income. Hard money lenders are private lenders who operate outside traditional banking regulations, allowing for faster closings and more flexible underwriting.

Expect terms of 6 to 24 months, interest rates ranging from 9% to 14%, and origination fees of 1 to 4 points. Hard money financing is best for:

Properties that do not qualify for conventional loans

Deals requiring a close in under two weeks

Borrowers with non-traditional income or limited credit history

The cost is high, so hard money works only when speed or deal access outweighs the expense. Always have a defined exit before committing.

Portfolio Loans, Credit Unions, And Other Flexible CRE Loan Options

Portfolio loans are held on the lender's balance sheet rather than sold on the secondary market. This gives the commercial lender more discretion in structuring terms, LTV, and qualification criteria. Community banks, credit unions, and some alternative lenders offer portfolio lending.

Credit unions often provide competitive rates and personalized service, especially for local or regional deals. Non-bank lenders and alternative lenders fill gaps that traditional banks leave open, particularly for borrowers with unique property types or less conventional financial profiles.

These flexible CRE loan options are worth exploring when your deal does not fit neatly into a standard bank or CMBS box. The lender relationship matters more here, so expect to invest time in finding the right partner.

Portfolio Loans, Credit Unions, And Other Flexible CRE Loan Options

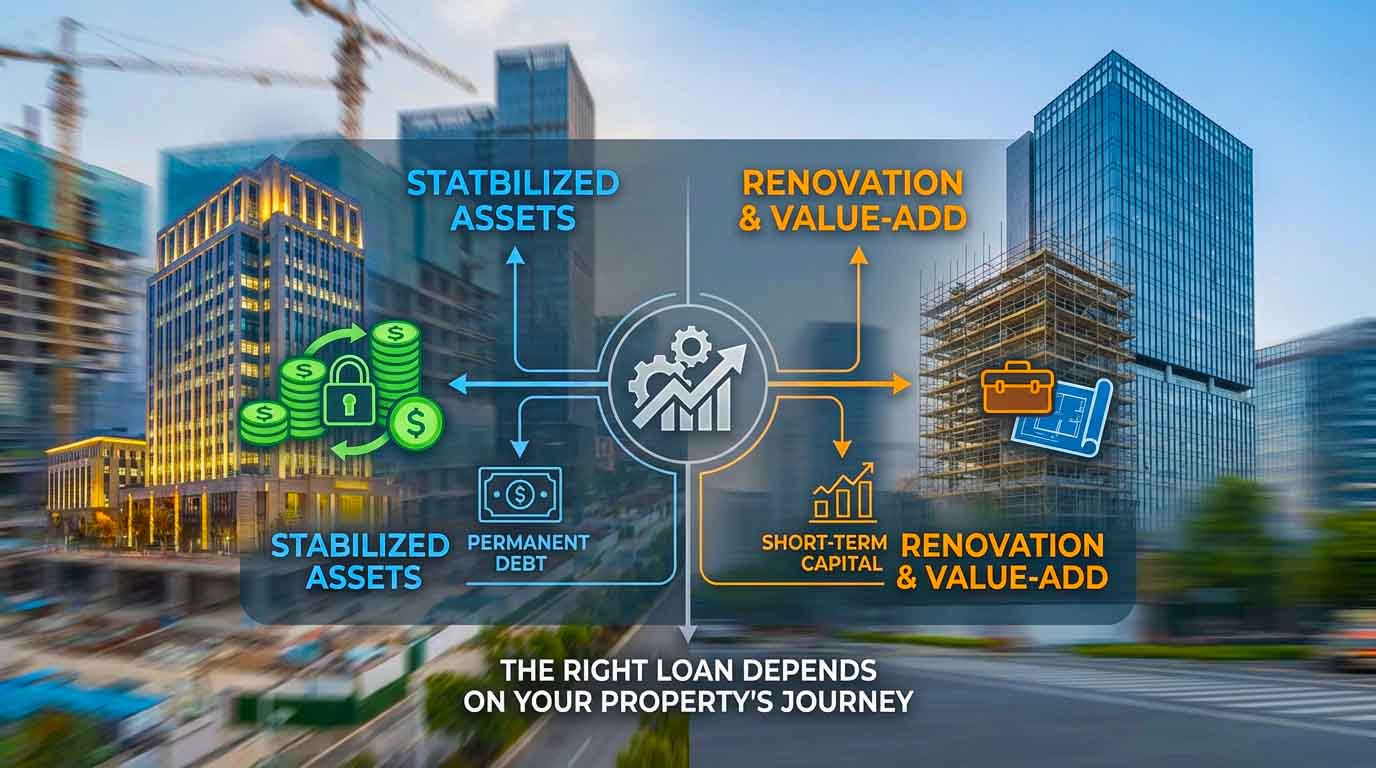

The right loan depends on where your property sits today and where you plan to take it. Stabilized assets generating steady income call for permanent, low-cost debt, while a vacant building targeted for renovation requires short-term, flexible capital with a clear refinance path.

Stabilized Properties Seeking Permanent Financing

If your property has strong tenant quality, high occupancy rates, and predictable cash flow, you are in position for permanent financing at the most competitive rates available. Conventional term loans, CMBS loans, and SBA 504 loans are your primary options here.

Focus on locking in a fixed rate, extending the amortization period to reduce monthly payments, and minimizing recourse exposure. CMBS offers non-recourse protection but limits flexibility. A traditional bank loan may require a personal guarantee but allows more control over the asset during the loan term.

Match the loan term to your hold period. A 10-year fixed-rate CMBS loan is efficient if you plan to hold for a decade. A 5-year bank loan works if you anticipate selling or refinancing sooner.

Value-Add Acquisitions And Short-Term Capital Needs

Value-add deals require short-term capital that allows you to reposition the property, increase rents, or improve occupancy before refinancing into permanent debt. Bridge loans and hard money loans are the standard tools.

Structure your financing to cover acquisition and renovation costs, with a realistic timeline for stabilization. Most bridge lenders offer interest-only payments, which reduce cash burn during the renovation phase.

Your exit strategy is the most critical element. Lenders will want to see a clear path to either a refinance at stabilized value or a sale. Underwriting on value-add deals leans heavily on projected income, not current performance.

Construction Loans For Ground-Up And Major Renovations

Construction loans fund ground-up development and major renovation projects through a draw schedule tied to construction milestones. The lender disburses funds as work is completed, and the borrower typically makes interest-only payments during the construction period.

Terms run 12 to 36 months, with rates above permanent financing. You will need detailed construction plans, a strong general contractor, and a clear plan to take out the construction loan with permanent financing or a sale upon completion.

Most construction lenders require 20% to 35% equity in the project. Expect rigorous inspections at each draw stage.

Office Buildings, Retail Centers, And Warehouses

Property type shapes your financing options. Lenders assess risk differently across asset classes.

Property Type

Lender Preference

Key Considerations

Office buildings

Moderate appetite; depends on lease terms

Tenant quality and lease duration drive underwriting

Retail centers

Selective; anchored preferred

Occupancy rates and tenant mix matter most

Warehouses

Strong demand from lenders

Industrial assets benefit from e-commerce tailwinds

Warehouses and industrial properties generally attract the best terms in 2026 due to sustained demand. Office and retail deals require stronger fundamentals and may face tighter LTV limits.

Seller Financing, Equity Partners, And Alternative Financing Structures

Not every deal fits a traditional loan structure. Seller financing, where the property seller acts as the lender, can bridge gaps in qualification or provide more favorable terms.

Equity partners contribute capital in exchange for an ownership stake, reducing your debt load but diluting your returns. This approach works well for large projects where leverage alone is insufficient.

Alternative financing structures, including mezzanine debt and preferred equity, allow you to layer capital above your senior loan. These tools increase your total leverage but add complexity to deal structuring and repayment priority.

Use these strategies when conventional lending leaves a gap, not as a first choice.

Seller Financing, Equity Partners, And Alternative Financing Structures

Commercial mortgage rates in 2026 reflect a stabilizing interest rate environment, with the Federal Reserve's target range holding at 3.50% to 3.75% and the 10-year Treasury hovering near 4%. The spread you pay above these benchmarks depends on your loan type, property risk, and borrower profile.

What Drives Commercial Mortgage Rates

Three primary factors determine your commercial real estate loan rates:

Benchmark rates: Most CRE loans price off the SOFR (Secured Overnight Financing Rate), the prime rate, or the 10-year Treasury yield.

Risk premium: Lenders add a spread based on property type, occupancy, borrower strength, and loan structure.

Market conditions: Lender competition, capital availability, and economic outlook influence how aggressively lenders price deals.

A stabilized multifamily property with strong DSCR might price at a tight spread over the 10-year Treasury. A transitional office building with uncertain leasing might carry a spread 300 to 500 basis points wider.

Fixed-Rate Versus Floating-Rate Loan Structures

A fixed-rate loan locks your interest rate for the full term, providing payment certainty and protection against rising rates. CMBS loans, SBA 504 loans, and many conventional term loans offer fixed-rate options.

Floating-rate loans adjust periodically based on a benchmark like SOFR or the prime rate. Bridge loans and construction loans are almost always floating-rate.

Choose a fixed rate when you plan to hold long-term and want predictable debt service. Choose a floating rate when your hold period is short and you expect to exit before rate movements become material.

Amortization, Balloon Payments, And Loan Terms

Most commercial real estate loans separate the term (when the loan matures) from the amortization (how payments are calculated). A common structure is a 10-year term with 25- or 30-year amortization, meaning monthly payments are based on a long payoff schedule but the remaining balance is due as a balloon payment at maturity.

Interest-only periods are common on bridge and construction loans, reducing cash outflow during the execution phase.

Understand your balloon payment exposure. If you cannot refinance or sell before the balloon comes due, you face a potential default.

Rate Lock, Prepayment Penalties, And Prepayment Structures

A rate lock freezes your interest rate between commitment and closing, protecting you from market movement during underwriting. Lock periods typically range from 30 to 90 days.

Prepayment penalties vary by loan type:

CMBS loans: Defeasance or yield maintenance; expensive to exit early

Bank loans: Step-down penalties (e.g., 5-4-3-2-1) or flat penalties

Bridge and hard money loans: Minimal or no prepayment penalties

Match the prepayment structure to your hold period. If you plan to sell or refinance within a few years, avoid loans with rigid prepayment structures that erode your profits.

Typical CRE Loan Rates By Loan Type

Loan Type

Rate Range (2026)

Typical Term

Conventional bank loan

5.50% – 7.50%

5 – 20 years

SBA 504

5.50% – 6.75%

10 – 25 years

SBA 7(a)

6.00% – 8.00%

Up to 25 years

CMBS / Conduit

5.36% – 7.00%

5 – 10 years

Bridge loan

7.00% – 12.00%

6 – 36 months

Hard money loan

9.00% – 14.00%

6 – 24 months

Portfolio loan

5.75% – 8.00%

5 – 15 years

Rates reflect general market conditions as of early April 2026 and vary by lender, borrower, and deal specifics.

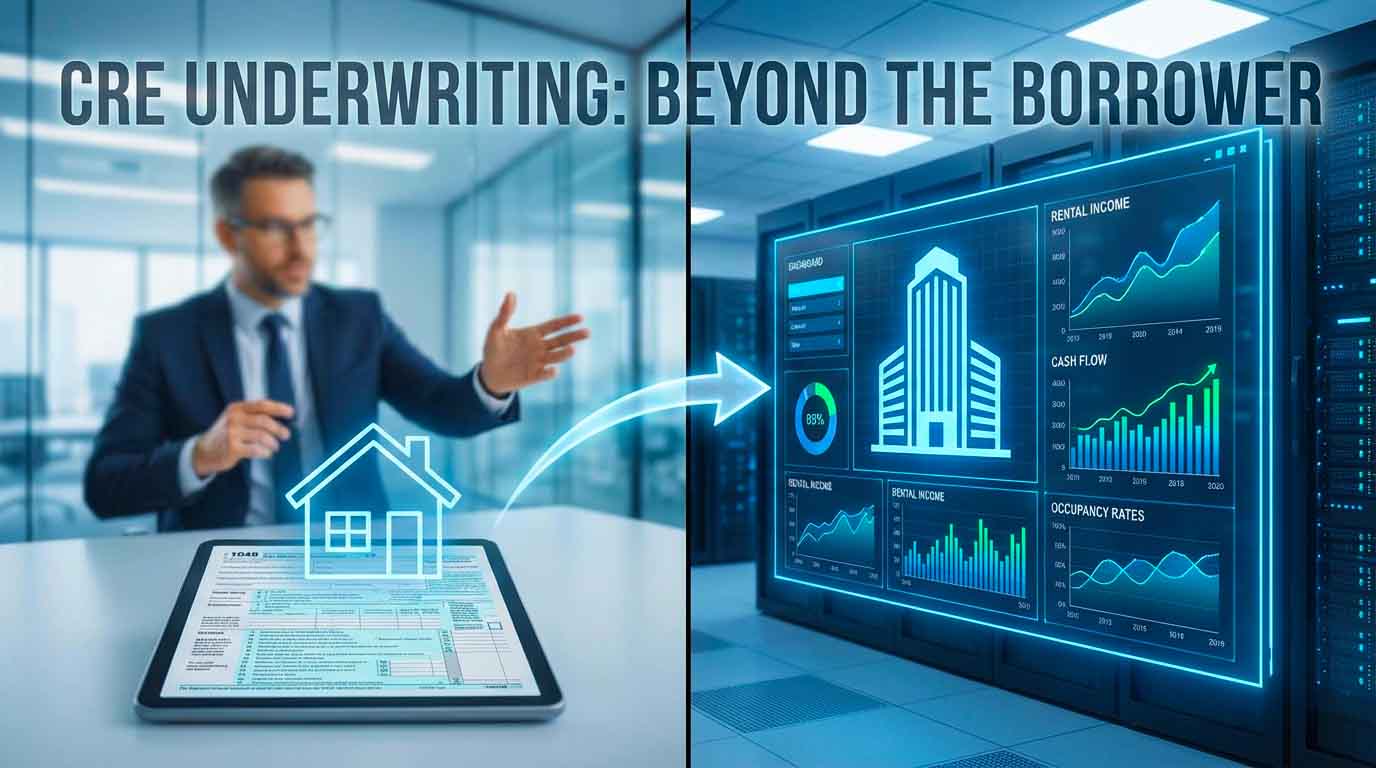

Qualification Standards And Underwriting Criteria

Commercial real estate lenders evaluate both the borrower and the property before approving a loan. Unlike residential mortgages, CRE underwriting places heavy emphasis on the income the property generates, not just your personal financial strength.

Credit Score, Cash Reserves, And Borrower Strength

Most commercial lenders require a minimum credit score of 660 to 680 for conventional financing. SBA loans may accept slightly lower scores with compensating factors, while hard money lenders often disregard credit scores entirely.

Cash reserves matter. Lenders want to see that you can cover 6 to 12 months of debt service plus any anticipated capital expenditures. Prior experience with similar property types strengthens your application significantly.

Strong personal and business financial statements, including tax returns, bank statements, and a personal financial statement, form the foundation of borrower evaluation.

DSCR And Debt Service Coverage Ratio Requirements

The debt service coverage ratio measures whether the property's net operating income (NOI) can cover the annual loan payments. Most lenders require a minimum DSCR of 1.20 to 1.35, meaning the property must generate 20% to 35% more income than the debt service.

DSCR = Net Operating Income / Annual Debt Service

A DSCR below 1.0 means the property does not generate enough income to cover loan payments. Lenders may still approve the deal if the borrower provides additional collateral or a strong personal guarantee, but expect tighter terms.

Loan-To-Value, LTV, And Down Payment Requirements

LTV measures the loan amount relative to the property's appraised value. Most commercial real estate loans require an LTV of 65% to 80%, meaning down payment requirements range from 20% to 35%.

Loan Type

Typical LTV

Down Payment

Conventional bank

65% – 75%

25% – 35%

SBA 504 / 7(a)

Up to 90%

10% – 15%

CMBS

Up to 75%

25%+

Bridge

65% – 80%

20% – 35%

Hard money

60% – 70%

30% – 40%

SBA loans offer the highest leverage for qualifying borrowers. Hard money lenders typically require the most equity.

Recourse Versus Non-Recourse Loan Structures

Recourse loans hold you personally liable if the property's sale proceeds do not cover the outstanding debt after a default. Most bank loans and SBA loans are recourse.

Non-recourse loans limit the lender's recovery to the property itself. CMBS loans are the most common non-recourse option. Standard carve-outs, called "bad boy" guarantees, still hold you personally liable for fraud, misrepresentation, or environmental issues.

Non-recourse protection reduces your personal risk but typically comes with higher rates, stricter qualification standards, and less favorable prepayment terms.

What Lenders Review Before Approval

The commercial loan underwriting process examines five core areas:

Property financials: Rent rolls, operating statements, lease terms, and occupancy history

Borrower financials: Tax returns, net worth, liquidity, and credit history

Appraisal and valuation: Independent assessment of property value and condition

Market analysis: Comparable sales, local vacancy rates, and demand trends

Deal structure: LTV, DSCR, loan term, and exit strategy

Prepare a complete loan package before approaching lenders. Missing documents slow the process and weaken your negotiating position.

How Investors Choose The Right Lender And Loan Structure

Selecting a lender is as important as selecting the loan product. The right commercial lender matches your deal timeline, property type, and long-term strategy. The wrong one costs you time, money, or both.

When To Use Traditional Banks Vs Alternative Lenders

Traditional banks are your best option when you have strong credit, a stabilized property, and time to navigate a thorough underwriting process. You will get the lowest rates and longest terms.

Alternative lenders, including non-bank lenders and private lenders, are better suited for deals that fall outside conventional parameters. This includes properties with below-market occupancy, borrowers with limited CRE experience, or transactions requiring a close in under 30 days.

Match the lender to the deal, not the other way around. Trying to force a transitional property through traditional bank financing wastes weeks and often ends in a decline.

Comparing Speed, Flexibility, And Cost Of Capital

Factor

Traditional Banks

Alternative / Private Lenders

Closing speed

45 – 90 days

7 – 30 days

Underwriting flexibility

Low

High

Interest rates

Lower

Higher

Documentation requirements

Extensive

Moderate

Relationship value

Long-term

Transaction-based

Speed and flexibility come at a premium. If your deal's profitability can absorb higher interest costs, a faster close from an alternative lender may produce a better net outcome than waiting for a bank approval that never materializes.

Planning Your Refinance And Exit Strategy

Every commercial real estate loan should have a defined exit. For bridge and construction loans, that means refinancing into permanent debt or selling the asset. For term loans with balloon payments, it means ensuring you can qualify for a refinance before maturity.

Start planning your exit 12 to 18 months before your loan matures. Track property performance, monitor rate trends, and maintain relationships with multiple lenders so you have options when the time comes.

Refinancing into a lower-rate product after stabilization is one of the most effective ways to increase cash-on-cash returns without additional equity investment.

Common Mistakes To Avoid In 2026 CRE Financing

Ignoring prepayment terms: Selling or refinancing early with a yield maintenance clause can cost tens of thousands of dollars.

Underestimating closing timelines: Bank loans routinely take 60 to 90 days; plan your purchase agreement accordingly.

Overleveraging: High LTV ratios reduce your margin of safety if property values decline or vacancy increases.

Skipping the exit plan: Entering a bridge loan without a clear refinance path creates unnecessary default risk.

Choosing rate over fit: The lowest rate means nothing if the loan structure restricts your ability to execute your business plan.

Frequently Asked Questions

The primary options include conventional bank loans, SBA 504 and SBA 7(a) loans, bridge loans, CMBS (conduit) loans, hard money loans, and portfolio loans. Each serves a different investor profile and property type, ranging from stabilized assets to transitional and ground-up projects. Your choice depends on property condition, timeline, and borrower qualifications.

Fixed-rate loans provide payment certainty and are best for long-term holds where you want to lock in debt service costs. Floating-rate loans adjust with benchmarks like SOFR and work better for short hold periods or when you plan to refinance before rate resets become material. In 2026, with rates relatively stable, fixed-rate products offer a strong value proposition for buy-and-hold investors.

Most conventional lenders require a 20% to 35% down payment, a DSCR of 1.20 to 1.35, and a credit score of 660 or higher. SBA loans allow down payments as low as 10% for qualifying owner-occupants. Hard money lenders may require 30% to 40% equity but place less weight on credit scores, focusing instead on property value.

SBA 7(a) loans offer more flexible uses, including acquisition, refinancing, and improvements, with variable or fixed rates and terms up to 25 years. SBA 504 loans are fixed-rate, limited to purchasing or improving fixed assets, and involve a Certified Development Company. Choose the 7(a) for flexibility and the 504 for rate certainty on a straightforward property purchase.

Expect to provide two to three years of personal and business tax returns, a personal financial statement, bank statements, a current rent roll, property operating statements, and a detailed business plan or deal summary. Lenders also require a third-party appraisal and environmental assessment. Having a complete loan package ready before approaching lenders accelerates approval.

Compare each term against your investment timeline and risk tolerance. Lower LTV means more equity at risk but better rates. Longer amortization reduces monthly payments but increases total interest. Non-recourse loans protect personal assets but cost more. Prepayment penalties should align with your planned hold period. Model each scenario against your projected cash flows to identify the structure that maximizes returns while managing downside risk.

At Dena Capital, we revolutionize the commercial real estate industry by investing in our people and technology to deliver unmatched client experiences and maximize value.